Allotments

An Agency's "Spending Plan"

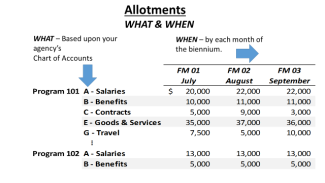

Understand

Agency allotments are often referred to as the agency's "spending plan". They are the agency's plans for what to spend their limited recourses on and when to incur these expenses. Good allotment planning allows management to make confident decisions, knowing that resources will be available when needed to support these decisions.

Additionally, allotments serve as a measuring stick upon which to compare actual expenditures and revenues. Differences between allotments (planned expenditures and revenues) and actual expenditures and revenues are referred to as variances. Agencies are expected to monitor variances and to take management action as appropriate.

Per OFM's allotment instructions, allotments are a detailed plan of expenditures authorized in the budget, the assumed revenue estimates, and the related FTE estimates. Allotments must:

- Conform to the terms, limits or conditions of legislative appropriations.

- Reflect the priorities of the agency's strategic plan, the implementation of those strategies, and the achievement of performance targets.

- Serve as the agency's best estimate of how their authorized expenditures will be spent and the revenue it will earn each month of the biennium.

Allotments, or the agency's "spending plan", should be considered policy and mirror the agency's strategic plan. For example, if an agency's strategic plan includes public outreach, resources should be clearly allotted to expenditures that support that outreach.

Allotment plans are reviewed by OFM, and upon approval, remain accessible and are monitored by both the executive and legislative branches, as well as the public. This monitoring helps ensure appropriations are used only for purposes that meet legislative intent, sufficient funding exists to allow the state to incur financial obligations, and changes in the original budget assumptions are communicated and understood. Adjustments to approved allotments may be submitted to OFM quarterly.

Initial allotments are typically due to OFM in early August after the biennial budget is passed. Refer to these Accounting and Budget Dates of Interest for specifics.

Take Action

Strategic Planning:

- Review your agency's strategic plan and think about what resources will be necessary to complete those objectives.

- Know your limitations; allotments may not exceed the terms, limits or conditions of legislative appropriations. Decide what priorities your agency will focus on and will likely allot resources to. Subsequently, decide what actions may be reduced or streamlined to conserve resources.

Build Your Allotments:

- Work with your SAFS budget analysts to build an allotment plan that matches your agency's priorities.

- Allotments are entered into The Allotment Systems (TALS) by your assigned SAFS budget analyst after agency approval. Once entered, allotments are sent to OFM for review and approval.

Monitor and Adjust:

- Review monthly budget status reports and seek to understand any material variances between actual expenditures/revenues and allotments.

- Increase or decrease agency spending, choices, or activities as necessary to ensure agency objectives are completed while remaining under appropriated spending levels.

- Adjust allotments, if needed or desired, to re-align your agency's budget plan to meet new challenges or updated strategic objectives. Work with your SAFS budget analyst to complete an allotment adjustment. Adjustments to approved allotments may be submitted to OFM quarterly.